Managing your cash flow is always a challenge for small businesses, and it’s more important than ever to work on this. Here, we’re sharing three key ways you can do this: reducing costs, generating cash, and empowering your team.

If your brick-and-mortar store is closed or you can’t make your product because your supply chain has collapsed, or you can’t fulfill customer orders, your incoming cash plummets, you could be in a state of negative cash flow during COVID-19. That means you have more cash leaving your business—whether that’s through paychecks, rent payments, paid marketing campaigns, and other fixed or variable costs—than you have coming in. That’s a problem, but it’s not a unique one. Even in a thriving economy, studies show that 82% of small businesses that fold do so due to cash flow issues.

Intuit released its State of Payroll in early 2020, with a focus on small business cash flow.

Given today’s market, though, working towards positive cash flow could be one of the most high-impact tasks you can do in the coming months to preserve your business’s future.

To help you improve your cash flow, we’re going to share three principles to follow when managing your cash flow:

For each, we’ll talk about how it helps with managing cash flow now, plus we’ll take a look at some examples of what you can do to make a difference for your business today.

If you’re a small business owner, rethinking your business finances was probably one of the first things you did in March after ensuring your team was safe. If you applied for a PPP loan, you’ve recently reviewed your financials in a level of detail that many of us don’t reach outside of tax season. But even if you have, you’ll want to continually re-examine your financials for the time being. And if you haven’t tackled this yet—or you’re taking this on for the first time due to downsizing here are some tasks you’ll want to check off your list right away.

First, in case it’s helpful, let’s review the definitions of fixed versus variable costs.

Depending on your business model and industry, it’s frequently easier to cut variable costs than it is fixed costs, so tackle those first. Can you find an alternate, less expensive way to ship your products? Can you temporarily cut your sales personnel’s commission and incentivize them in a different way? But also think through how you can actually change fixed costs into variable ones. When all else fails, try following in the footsteps of one entrepreneur, Brad Emerson, and cut literally anything you don’t need. During the Great Recession, he cut not only maintenance and computer costs, but also air conditioning. If there’s a time to practice running a lean business, it’s now.

If this process of reviewing line items and determining where to make cuts is new to you, the SBA’s free worksheet and Entrepreneur’s break-even calculator can help you get started.

Our economy is an ecosystem; the people and entities that you buy supplies or rent property from depend on your business, so helping to preserve your business solvency is in their best interest. So, for example, if your business is going to have trouble paying rent, have a frank, virtual face-to-face with your landlord as soon as possible. When you do, be sure to be totally honest about what you really need right now versus the assistance you anticipate needing in the future. If you really can afford to pay your rent right now, but anticipate struggling in two months, don’t burn your bridges by asking for a pass on your rent this month. Letting your landlord help other, more immediately needy tenants this month—and saving them a ton of stress—you’ll not only preserve your access to the assistance you need when you do need it, but also your integrity will only benefit your business for years to come.

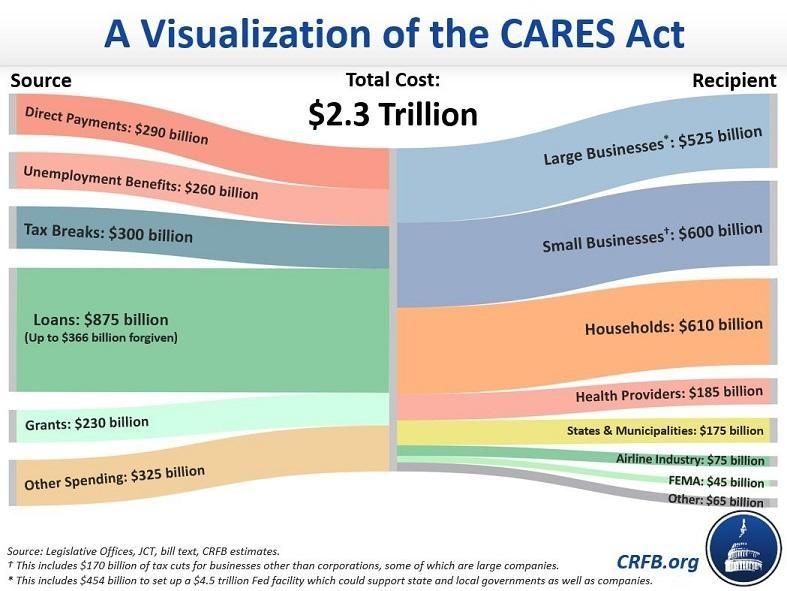

Between the emergency funding provided by the Federal government’s CARES Act, grants offered by corporations like Facebook and Google, and donation-driven funds at the local level, there’s more than likely an available funding option that’s well suited for your business. Using a loan to inject cash into your business may seem like taking drastic steps, but it could mean the difference between having to totally rebuild your business during a recession and preserving a strong foundation to work with for the months ahead.

So explore the SBA’s catalogue of resources and Inc.’s helpful list of small business loan and grant options to brainstorm what might work for you, and contact your local city government to see what programs it’s launched or have planned.

Now’s the time to audit your catalogued invoices for any that are due but remain unpaid—a thankless task when the economy is doing well, but a thoroughly necessary one now. If you haven’t yet, contact any customers or partners who owe you money right away and, again, have a human, empathetic, honest conversation with them. Give them the opportunity to be forthright about their own business situation and needs. If they need the help and you can manage it, consider extending their invoice’s due date. If they don’t need the help, take the opportunity to prompt a timely payment—your balance sheet will thank you.

Profit is total sales minus the total cost of producing those goods (your variable costs). Profit doesn’t equal positive cash flow and, remember, what you need right now is cash.

Refocusing on generating cash can definitely be a mental shift, but if you’ve already tackled the top-priority tasks to strengthen your cash flow (e.g., cutting variable costs), many of your usual profit-generating actions can be adjusted or reprioritized toward the goal of generating cash.

For example, you’ve probably seen that many brick-and-mortar businesses are currently marketing their e-gift cards. While gift cards aren’t a new revenue stream for many businesses, they’re not usually something you’d put a lot of marketing effort behind, except perhaps as a “last chance” campaign targeting anyone who’s forgotten the next big holiday. But pivoting to focus on gift cards right now is an easy low-cost, low-effort way to get more cash in the door right away—without having to spend cash on the raw materials and other supplies needed to actually create your product or service (i.e., your variable costs).

Here are some more ideas to try.

Acquiring a net new customer is always more expensive than driving sales from prior or existing customers. In the current market environment—with millions of Americans unemployed and hesitant to spend money, and millions of others are working from home and desperate for distractions—it’ll be harder than ever to convert new business. But if you’re a consumer brand, your existing customers are likely bursting with pent-up demand. If you offer the right discount at the right time with compelling “exclusive” messaging, you’ll likely boost sales, generate cash, and promote customer loyalty. Also, if you sell a physical product, clearing out some of your inventory could help you cut back on rental or storage costs.

Many products are generally sold to businesses with office space (e.g., office furniture) or that reach consumers via a middleman (e.g., Target)—perhaps yours included! Empower your marketers to whip out their rebranding ideas and pull together a simple landing page to get your product in front of consumers. For example, the team behind HUNGRY@Home is used to catering corporate events, but these days, they’ve pivoted to cooking and delivering healthy, safe, affordable family-style to people’s homes.

HUNGRY@Home’s offering.

If you can, change your offering to the new needs of your post-pandemic customers. Consider offering products or services that offer high profit margins, economies of scale, and tried-and-true ways to collect payment. Whew! That was a lot. Let’s break that down:

As Shopify points out, with Amazon prioritizing the delivery of groceries, diapers and infant formula, and personal care items, your local business might find an opportunity to step into that gap by providing faster, contactless delivery for beach reads, summer clothing and gear, home repair equipment, and other non-necessary, but definitely helpful products.

Experiment with offering these products to existing customers at a discount, offering free or discounted delivery, or other offers to discern how to drive the most ongoing local demand while generating the most cash for your business.

We’re all saying it so often these days that it’s already become cliche: “We’re all in this together.” We’re saying it, though, because it’s so widely applicable, whether you’re talking about protecting ask-risk neighbors or preserving your small business.

As a business leader, now is not the time to hide in your office—or behind your laptop screen at home. It’s time to step up and lead—by empowering your employees to step up as well.

How? First, be transparent about your real business metrics and what you need to achieve. In ordinary times, establishing a business objective that the whole organization can work toward together can generate a shared sense of mission, promote teamwork, and foster individuals’ pride in the business’s accomplishments. It’s natural, though, to hesitate about sharing metrics during a crisis like this, especially if your business goals from the booming start to the year have likely been thrown out the window. But if you are open about what needs to happen to keep the business afloat—and about your cash flow goals, in particular—you communicate how much you respect and trust your employees, and you empower them to work together to address those goals.

Being transparent about metrics and open to new ideas can also boost employee engagement, which is good for business.

To truly empower your team, you’ll also want to make sure that your employees all understand what the metrics mean. Show your team a P&L and explain how it works. Walk them through a balance sheet. Describe the difference between profit and positive cash flow, and why positive cash flow is the current priority.

But most importantly, make sure each person on your team understands where they personally drive business impact. As a marketer at a small business, my prior employer created a huge chart of where cash came in and went out; we each wrote our tasks on post-its and took turns placing the post-its on the chart to indicate where and when our everyday work impacted the business. Thanks to this incredibly helpful exercise, we all walked away with a far firmer grasp of how we could each make a difference. Try doing something like this virtually, with a Google doc or other tool. Tell your team to raise their hand immediately if they have an idea to improve cash flow, and emphasize that all ideas are good ideas, and everyone’s job is impactful and relevant.

By taking the time to educate and empower your team, you’ll invest deeply in your team’s resilience and make huge strides toward unleashing their creativity and motivation to address your business’s challenges. Because we really are all in this together.

Whether or not this particular economic crisis is your first rodeo, this is far from the first time that small businesses like yours have faced this level of uncertainty. As it so happens, we experienced one pretty recently—and the lessons learned in 2008, whether about cash flow management or any other business or leadership skill, are still incredibly valid.

So as you work on improving cash flow with these tips, keep in mind what worked before—and listen to your colleagues or your business partners about their experiences. Reach out to small business owners and entrepreneurs in your network, and ask them what they did in 2008. Read about the experiences of Brad Emerson and so many others. Research not just how businesses in your industry responded, but how your partners’ industries and verticals made their way. You can even get your whole team involved: In a shared place, document what you find, both what worked and what didn’t work. Review your findings together, and discuss how they support or undermine your potential path forward. The solution to your cash flow struggles could be unlocked just by asking a fellow small business owner a few questions.